By

Lachezar Kolev & Andrea Candela

September 15, 2025

10 Min Read

Proprietary AMMs (Prop AMMs) are a new breed of liquidity venue on Solana that differ sharply from traditional public AMMs. Instead of relying on crowdsourced liquidity and transparent bonding curves, they use private vaults, off‑chain quoting engines, and tight integration with aggregators like Jupiter to deliver lower latency, tighter spreads, and greater resistance to MEV. This article explores what they are, why they emerged, how they work (to the extend that is possible to know), and what their rise means for Solana’s market structure.

To understand Prop AMMs, one must first understand the foundational layer on which they are built: the blockchain virtual machine. A virtual machine (VM) is the runtime environment that executes smart contract code, effectively acting as the “brain” of the blockchain. On Solana, this is referred to as the Solana Virtual Machine (SVM). The design of the SVM dictates everything from transaction costs and speed to the very patterns developers use to build applications. Here’s a simplified overview.

Solana was designed from the ground up to prioritize performance and throughput. While it employs a Proof-of-Stake (PoS) consensus layer, it introduces a key innovation called Proof of History (PoH). PoH is not a consensus mechanism itself but a cryptographic clock that provides a verifiable ordering of events, which Tower BFT (a PoS‑based consensus protocol) then uses to finalize blocks. This combination enables massive parallelization of transaction processing and lower coordination overhead.

Solana's runtime design and architecture offers a fundamentally different approach to transaction processing, which in turn fosters a very different developer and user experience for complex operations.

The SVM allows a single Solana transaction to contain multiple, independent instructions targeting different on‑chain programs. Each transaction is atomic: either all instructions succeed, or the entire transaction fails and no state changes are made.

This base-layer atomic composability shifts how arbitrage is executed. An arbitrageur on Solana does not need to deploy and call a special proxy router contract. Instead, they can construct a transaction off-chain that includes all the necessary steps of their arbitrage strategy as separate instructions.

For example, a CEX‑DEX arbitrage might involve:

All of these steps can be bundled into one transaction and submitted directly. This makes dedicated on‑chain routers unnecessary, since they would only add extra cost and latency.

The key bottleneck on Solana is not execution efficiency, but the off‑chain computation required to discover optimal paths across fragmented liquidity. This naturally reinforces an aggregator‑centric model: specialized services focus on off‑chain route discovery and computation, while the SVM ensures atomic, low‑latency execution on‑chain.

This architectural divergence is one of the primary drivers behind the rise of this aggregator-centric model, where specialized services focus on off-chain computation to find the best possible trade routes for users.

The architectural advantages of the Solana Virtual Machine (SVM)—namely, its ability to atomically compose multiple instructions—have directly shaped its market structure. Unlike the EVM world where users often interact directly with individual DEX protocols like Uniswap, the Solana ecosystem has evolved into an aggregator-centric market.

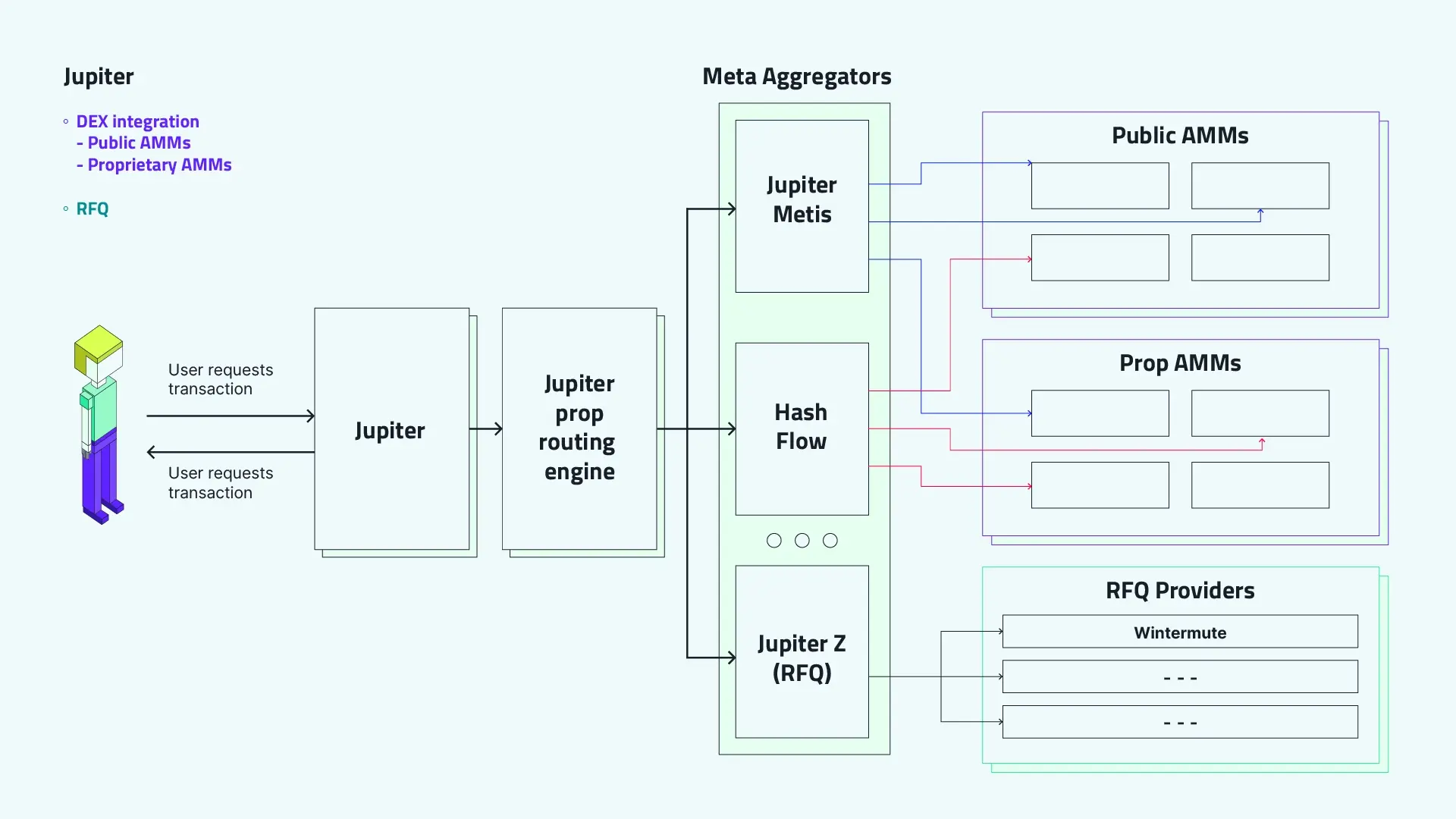

The current Solana market structure has a few primary retail entry points, most notably Jupiter and wallets like Phantom that route through Jupiter. These serve as dominant channels for retail order flow into on-chain liquidity, though institutional and direct integrations also exist.

Analysts such as Delphi Digital and Helius estimate that Jupiter is responsible for roughly ~80% of aggregator-related fees. This number is an approximation, fluctuates over time, and should be understood as fee share rather than absolute trade volume share.

Aggregators function as order flow coordinators and matching engines responsible for routing the user’s transaction. In Solana’s case, they not only query downstream liquidity sources but also optimize for compute unit efficiency - this is something to keep in mind since it is closely related to the rise of proprietary AMMs.

Every time a user requests a price quote from Jupiter, the meta-aggregator prompts downstream-hooked liquidity sources for current rates and, based on the responses, configures optimal routes.

Here’s a simplified scheme of Jupiter’s order flow.

The process of using an aggregator like Jupiter is seamless for the user but complex behind the scenes:

The aggregator model is a natural consequence of Solana's architecture. The ability to bundle the aggregator's potentially complex, multi-hop route into a single, atomic transaction is what makes the entire system feasible and highly efficient. In addition to composability, analysts such as Delphi Digital emphasize that aggregator dominance is also about minimizing MEV/LVR leakage and managing compute unit (CU) costs.

On an EVM chain, executing such a route would require a very complex and expensive custom router contract. On Solana, it is better described as a property of the SVM transaction model and fee/compute structure rather than a general “native feature” of the blockchain. This distinction matters, since it is the combination of atomic instructions and CU pricing that enables aggregators to focus on their core competency: off‑chain computation, oracle freshness, and route‑finding, without being bogged down by the complexities of on‑chain execution.

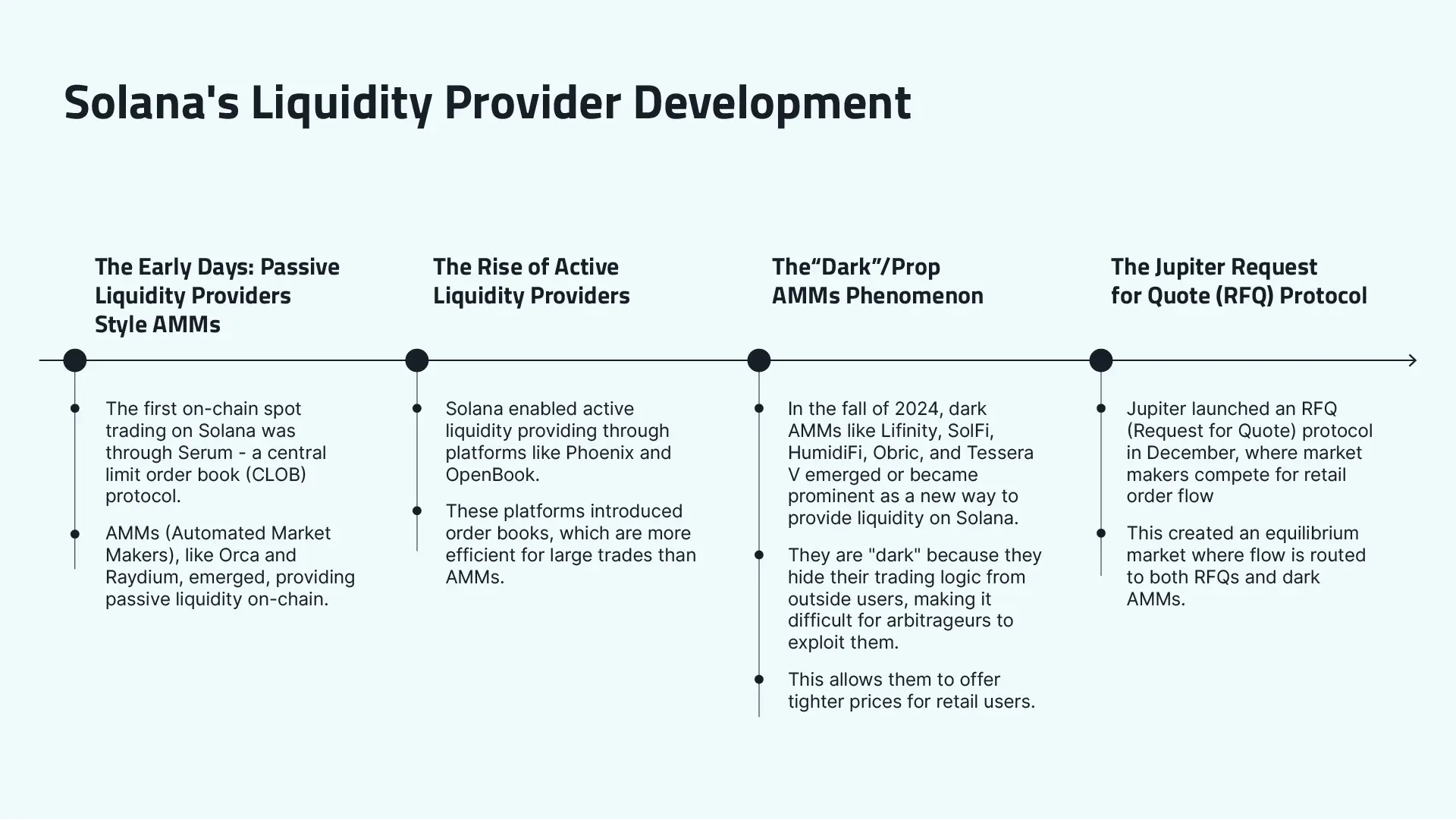

The current state of the Solana aggregator-centric market model evolved over time, shaped initially by strong retail activity but increasingly also by institutional flows and OTC integrations.

This leaves us with three main sources of on-chain liquidity on Solana, as supported by Helius, Delphi Digital, and other research sources:

While each model has its own intricacies, the focus here is to better understand Prop AMMs: what problems they solve, how they work (to the extent that we can know), what their characteristics are, what advantages they bring, some prominent examples, and what the implications are for Solana’s market structure.

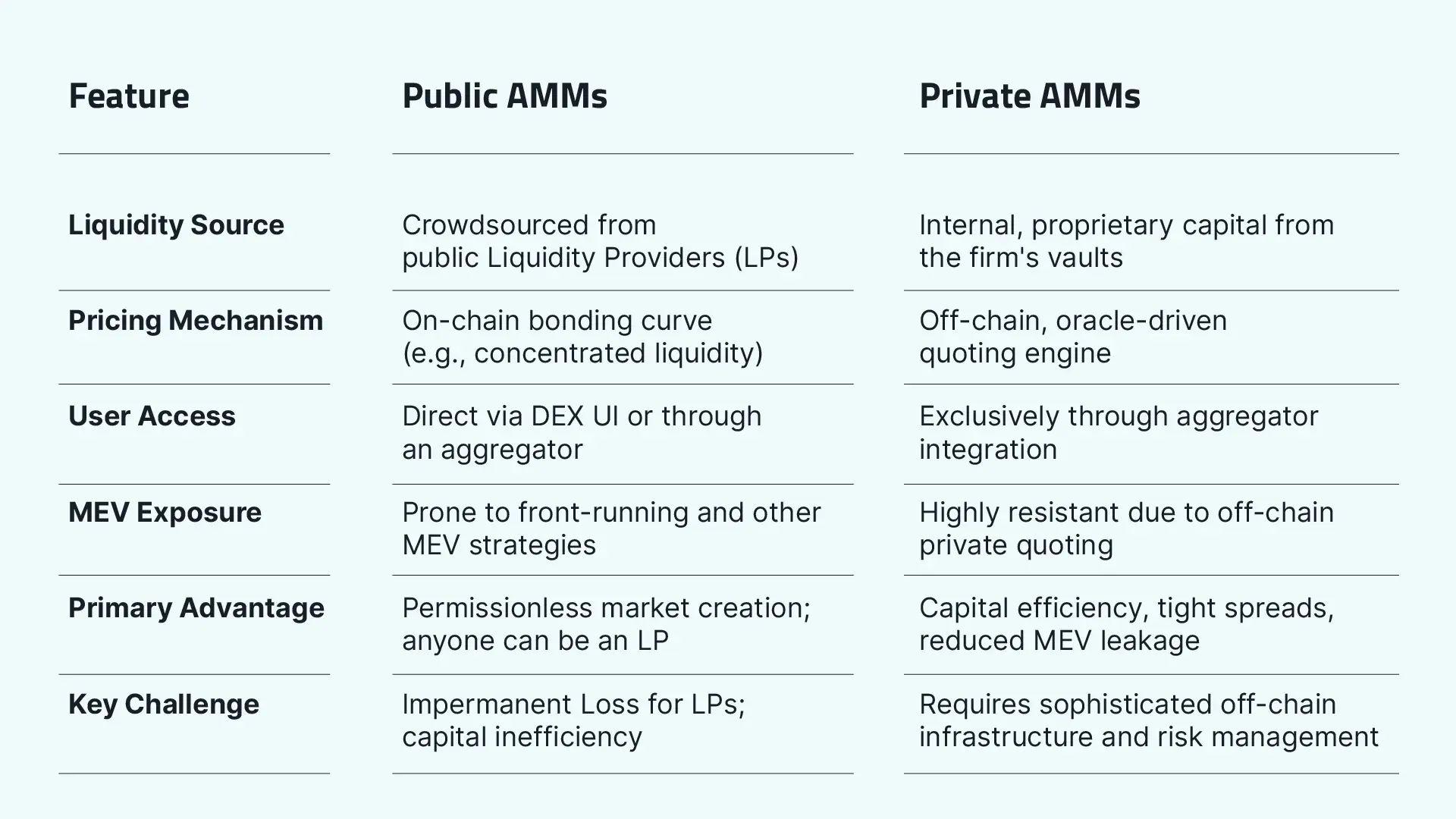

Solana’s fee structure is tied to compute units (CU). Each transaction can consume up to ~1.4 million CU, and each instruction up to 200,000 CU. Updating hundreds or thousands of live quotes on an order book can therefore be prohibitively expensive in terms of CU consumption. Proprietary AMMs sidestep this by allowing market makers to update a small set of variables in their smart contract, effectively shifting entire pricing curves with far less computational overhead.

Constant-product AMMs (x*y=k) and even concentrated-liquidity designs are limited by deterministic bonding curves. Prop AMMs instead define liquidity as a dynamic preference curve. This approach allows them to tune inventory around the oracle price, maintaining optimal balances while still achieving capital efficiency. This enables tighter spreads and reduces the risk of impermanent loss compared to passive LPs on public AMMs.

Traditional public AMMs expose all order flow, inviting MEV, front-running, and LVR leakage. Prop AMMs conceal execution paths and limit information leakage, making it harder for external actors to pick off quotes. The result is tighter and more stable pricing, lower latency, and deeper liquidity - all while keeping CU and fee costs manageable.

Prop AMMs trade from proprietary balance sheets held in private on-chain vaults, not crowdsourced LP capital. This capital is deployed selectively, usually on liquid pairs where spreads can be kept tight (e.g. SOL to USDC). Unlike public AMMs, these vaults are actively managed by professional firms, giving them flexibility to adjust inventory in response to market conditions. Some reports suggest that vaults may also be segmented across strategies (e.g., market making vs. hedging) and integrated with off-chain risk systems, aligning them closer to TradFi desk models. The lack of external LPs also means retail users do not capture fees, but instead benefit indirectly through tighter execution and reduced slippage when routed via aggregators.

When a user submits a trade through an aggregator like Jupiter, the aggregator embeds a cryptographically signed quote from the prop AMM. This signature authorizes the AMM’s on-chain program to execute the swap, moving funds from its internal vault to the user. This results in off-chain computation paired with minimal on-chain instructions, keeping CU costs low. In practice, these quotes are time‑sensitive and often expire within seconds to avoid stale execution. Some sources note that prop AMMs may also attach custom fee tiers or size limits, allowing them to manage risk dynamically. This design helps explain why they can consistently offer tighter spreads for larger trades compared to public AMMs.

Prop AMMs rely on high-frequency oracle updates to stay in sync with external markets. Lightweight developer frameworks like Pinocchio make oracle updates more efficient, and, as already mentioned, Solana’s CU pricing model incentivizes minimizing the compute required for each update. This approach requires keeping these updates fresh, since stale oracles widen spreads or even halt quoting. In practice, market makers often send frequent oracle transactions with high tip-per-CU bids to Jito validators, ensuring their updates are prioritized in block production. This mechanism helps prop AMMs maintain tight spreads and reduces the risk of stale quotes undermining execution quality.

Some research suggests that if oracle freshness decays even for a few blocks, spreads widen dramatically, essentially pausing effective quoting. This highlights how oracle latency is a core bottleneck for the competitiveness of prop AMMs.

These venues run sophisticated off-chain engines that continuously monitor centralized exchanges and public DEXs. This allows them to price in line with global markets while hiding their intent until execution. This concealment is what reduces MEV and toxic flow. In practice, the off-chain engines constantly ingest price feeds from CEXs, public AMMs, and oracles to ensure their signed quotes track global best execution. Quotes are typically short-lived (often expiring within seconds) to avoid being picked off, and may include dynamic size limits or fee adjustments to manage inventory risk.

When queried, the off-chain engine decides whether to return a quote. If it can beat public AMMs while remaining profitable, it returns a signed quote (price, size, expiry). This ensures traders only see executable quotes rather than passive, exploitable liquidity. These quotes are intentionally short-lived to minimize stale fills. They may also be size-gated or include adaptive fees, allowing the AMM to manage inventory risk dynamically. In some cases, prop AMMs can decline to quote altogether if market volatility is high or if their internal vault inventory is imbalanced, reinforcing that participation is discretionary and strategy-driven rather than passive.

Prop AMMs are operated by professional trading firms, not retail LPs. Examples often cited include SolFi, ZeroFi, Tessera V, HumidiFi, and Obric. These firms bring active risk management, co-location with validators, and proprietary strategies more akin to TradFi prop desks than to DeFi liquidity mining. Their role reinforces the shift from passive, community LPing toward professionalized market making that leverages Solana’s low-latency infrastructure.

Jupiter sits at the center of this system. Estimates suggest ~80% of Solana’s aggregator fees route through Jupiter. Its control over retail order flow indicates that Jupiter’s dominance not only shapes liquidity routing but also serves as a gatekeeper. This could potentially lead to slow listings of new venues. Some observers note that this concentration raises questions about centralization of order flow, though in practice it also standardizes UX for retail and ensures consistent access to both public and proprietary liquidity.

Proprietary AMMs are fundamentally dependent on aggregators for their business model. They do not operate public-facing user interfaces and do not compete for retail attention. Their entire strategy is to integrate on the backend with aggregators like Jupiter and compete purely on price. If a prop AMM chooses not to provide a quote for a particular trade (perhaps because it's too risky or unprofitable), it faces no penalty; the aggregator will simply route the user's order to the next-best option, likely a public AMM. This allows prop AMMs to be highly selective about which trades they fill. In practice, this selective quoting aligns with their risk management strategies, and sources note that aggregators sometimes even run mini-auctions among prop AMMs to determine who provides the best quote. This reinforces how tightly coupled their survival is to aggregator infrastructure and order flow control.

Because they are not exposing how their trading logic works to anybody outside of the aggregator, proprietary AMMs resemble dark pools in TradFi. Users cannot access a public-facing interface; all interaction happens through aggregators, which makes them opaque and difficult to audit. In addition, many of these programs are upgradable, meaning their operators can change logic over time without external notice.

For these reasons, prop AMMs are intentionally difficult to reverse engineer. Analysts note that this opacity protects against toxic flow and MEV extraction, but it also raises transparency and trust concerns compared to permissionless AMMs.

To gain a firm grasp of how proprietary AMMs differ, it can be useful to compare them side by side with public AMMs.

A major advantage of proprietary AMMs is their inherent resistance to certain forms of Maximal Extractable Value (MEV), such as front‑running or sandwich attacks. Because the price is determined and signed off‑chain for a specific user’s transaction, it is not broadcast publicly for MEV bots to see and exploit. An MEV bot cannot simply copy the trade or front‑run it because they do not have the required signature from the AMM’s off‑chain system. This reduction in MEV leakage allows prop AMMs to offer tighter spreads and more competitive prices to users, as they do not have to price in the expected cost of being arbitraged.

Prop AMMs can adjust quotes dynamically based on market conditions. Their off‑chain engines allow them to cancel or modify pricing in near‑real‑time, enabling them to provide the tightest price without exposing stale quotes.

Because execution is handled with lightweight on‑chain instructions and often co‑located infrastructure, prop AMMs achieve some of the lowest latency fills for end users. Jito bundles and validator proximity further reduce propagation delays, giving professional firms an edge in speed.

Since quotes are firm, signed, and only live for a short expiry window, users experience less variance in their fills compared to public AMMs, where execution can be influenced by slippage or MEV activity.

While inspired by dark pools, prop AMMs differ from traditional finance venues by being natively integrated with blockchain infrastructure. They combine privacy‑preserving execution with composability in DeFi, offering a hybrid model that does not have a direct equivalent in traditional markets.

Markets are ultimately a manifestation of human incentives and behavior, not pure ideology. Proprietary AMMs demonstrate this by importing professionalized, profit‑driven market making into DeFi. In many ways they resemble on‑chain hedge funds: private capital deploying strategies through opaque infrastructure. Some argue this is a return to TradFi patterns, while others see it as a pragmatic adaptation of DeFi to meet institutional‑grade execution needs.

What seems clear is that this development opens up significant opportunities for quant trading teams to diversify revenue by operating prop AMMs on‑chain. At the same time, it raises open questions about transparency, access, and whether aggregator‑dominated order flow represents a new form of centralization within DeFi.

Proprietary AMMs are a new type of liquidity venue on Solana that operate differently from traditional public AMMs. Instead of relying on crowdsourced liquidity from public LPs and transparent bonding curves, Prop AMMs utilize private on-chain vaults with capital actively managed by professional trading firms. Their pricing is determined by sophisticated off-chain quoting engines rather than fixed on-chain curves.Key differences include:

Solana's architecture, particularly the Solana Virtual Machine (SVM), plays a crucial role in enabling Prop AMMs and the aggregator-centric market.

Prop AMMs address several key challenges within the Solana ecosystem:

Prop AMMs blend sophisticated off-chain infrastructure with minimalist on-chain execution logic:

Prop AMMs are considered "dark" because their trading logic and execution paths are opaque, resembling dark pools in traditional finance.

Implications:

For traders, Prop AMMs offer several significant advantages, primarily driven by their design:

Jupiter acts as a central matching engine and the dominant retail entry point for order flow in the Solana ecosystem.

Implications of Jupiter's Dominance:

Or just shoot us a message on Telegram